2016 is going to be a very different year compared to the past few years. The phrase “global war on terror” was first used by U.S. President George W. Bush after the September 2001 attacks. That term was removed from regular communication by the Obama administration in 2009. It might just come back in 2016, though, as next year seems to have all the ingredients for a fairly violent year.

The Fed is expected to start on an upward trajectory for interest rates. This will have significant effects on the world economy as other central banks may or may not follow suit. Rising rates will also have an impact on the U.S. dollar, commodity prices, corporate earnings and the stock market. Significant emerging economies, like China, India and South Korea, have all recently cut their own interest rates to gain back the momentum they’ve lost in the last three years. This will have a counterbalancing effect on rising interest rates.

The following trends will help investors decide the best course of action as they plan for the new year.

1. Global GDP Might Break Free in the Second Half of 2016

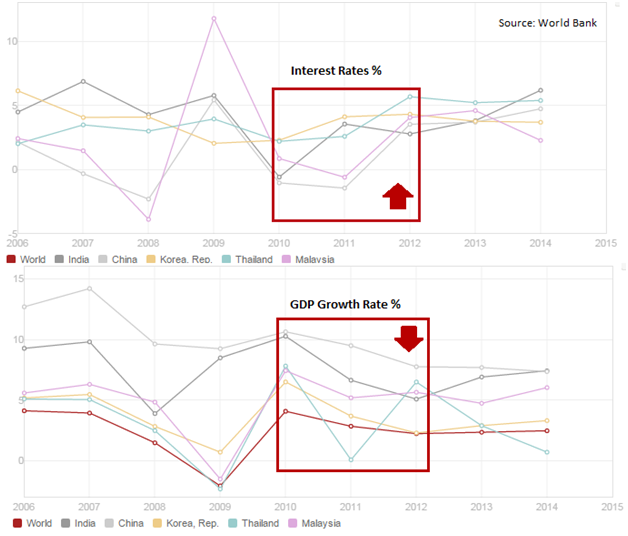

While most analysts are obsessing over interest rates in the U.S., there is an interesting correlation being missed: interest rates and GDP growth rates of emerging economies. World GDP grew 3.8% in 2015. To put things in perspective, world GDP has grown between 3.3-3.4% from 2012 to 2014. This is far from the 5.4% growth it experienced in 2010 but is still an improvement from the flat trajectory of last three years. The same is observed in emerging economies. GDP growth rates for emerging economies have been steadily falling, from 7.5% in 2010 to 4.4% in 2014. However, 2015 seems to have broken the pattern and emerging economies rallied to grow 5% (led by India, South Korea and Malaysia).

An interesting point note in the graph below is that falling GDP growth coincides perfectly with increasing interest rates in those economies (which usually happens).

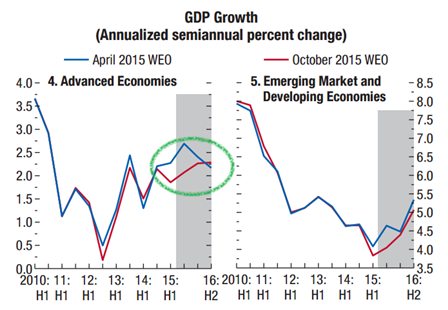

A few significant emerging economies have reduced their interest rates recently (including China, India, and Taiwan), which is likely to provide a push for global demand. World GDP growth is demand-driven by developing countries. This, along with the steadily growing growth rates of advanced economies and the euro zone, offers a ray of hope for 2016. This is reflected in the World Economic Output report published by the IMF. There is a change of GDP outlook between the two reports published in April and October (green highlighted area in the graph below).

2. Global Defense Spending Will Rise Sharply in 2016

This year has unfortunately been full of domestic and international violence. Take a look at some of these stats:

There have been more than 900 mass shootings since the beginning of 2013.

More than 1,000 people have been killed by police in the U.S. (in 2015 so far). This has resulted in a push for reforms in police action (e.g. the use of body cameras).

There was an 80% increase in terrorism deaths between 2013 and 2014. 2015 has been a particularly violent year, so the numbers might prove to be even more than 2014.

ISIS has proved to be one of the most brutal and wealthy terror groups to have challenged the world. The Western world has taken time to react to their threat, but they now control large areas of Syria and Iraq. The group reportedly brings in more than $500 million a year from oil alone. Estimates on the number of fighters have varied from 20,000 to more than 100,000. As a result, hundreds of thousands of people have been displaced from Syria and Iraq.

What does this mean for investors? Because wars in the Middle East disrupt oil supply, it might lift oil prices. Defense-related spending will go up both in the U.S. and globally. These include multiple product categories, such as tanks, navigation systems, body cameras, drones and monitoring systems.

3. Pressure on Oil Will Continue in the First Half of 2016

Oil breached the $40 per barrel mark in early December for the second time this year. There have been conflicting reports about whether or not OPEC will cut production. Supply has continued to rise even though countries are now under pressure to cut production. As per a senior OPEC delegate, Saudi Arabia will be proposing a cut of 1 million barrels per day, but it is not clear if other OPEC members will agree. As per current estimates, supply outstrips demand by more than 1 million barrels a day. It is expected that demand will be slower than usual this winter due to the El Nino effect. Even if OPEC cuts its supply, there are other drivers that are likely to pull oil prices back. If the Fed raises interest rates and the dollar continues to dominate, for example, oil prices will be under pressure. The situation, however, will change if OPEC decides to cut down supply and/or demand from emerging markets starts to pick up pace. Even if that were to happen, it will only be in the second half of 2016.

4. 2016 Might Be a Mixed Year for the Stock Markets

From the depths of the market low in early 2009, the S&P 500 has risen nearly 200%. That’s remarkable when you consider that it’s been less than six years since then. In the meantime, U.S. government debt to GDP has grown by 25%, inflation has been patchy, the GDP growth rate has been patchy, and the U.S. dollar has been rising steadily (which is not a good thing when you are coming out of a recession), and all this despite low interest rates. An even better picture is painted by the graph below. While U.S. corporate profits have been on a sideways track since 2012, the Dow Jones has had a steady upward trend. This should scare you if you are heavily invested in the stock market as it is clearly a sign of a bubble. If the stock market continue to go on a journey away from earnings, it is fair to expect a crash.

5. The Dollar Will Dominate Even More in 2016

With interest rates rising and commodity prices struggling (especially oil), the dollar is set to be even more dominant in the market. A dominant dollar certainly means that exports will be under pressure. The U.S. economic recovery, as much as the Fed would want it, can’t be export-driven if the dollar keeps rising against all major currencies. The dollar might have its own issues but other currencies have a life of their own too. For example, the yen and euro are facing downward pressure due to quantitative easing. This has, and will, keep putting more pressure on the U.S. dollar to go even higher. The Fed is worried about exports and might have started a currency war to protect its interests.

The Bottom Line

There are many anomalies to consider for 2016. There is an oil supply glut and yet no one seems to be cutting production. In the short term, oil prices will increase due to geopolitical conflicts in the Middle East.

U.S. corporate earnings have not grown as fast as the stock markets, meaning the market may need a correction to align itself to reality. Unemployment is down and there is a slight improvement in inflation and GDP growth. But an increase in interest rates might push them back. The dollar is already strong and commodity prices are in free fall. A higher interest rate is not going to help them either (of course these things can’t be decided in isolation). And yet the Fed is planning to increase interest rates this month.

All this must feel like heaven for traders and speculators because anomalies result in volatility. For investors, it is very important to keep on top of things. Maybe mutual funds are the answer? Active professional management is beneficial in uncertain times.

For more frequent updates follow me @tanmoyroy.

Sign up for Advisor Access

Receive email updates about best performers, news, CE accredited webcasts and more.

2016 is going to be a very different year compared to the past few years. The phrase “global war on terror” was first used by U.S. President George W. Bush after the September 2001 attacks. That term was removed from regular communication by the Obama administration in 2009. It might just come back in 2016, though, as next year seems to have all the ingredients for a fairly violent year.

The Fed is expected to start on an upward trajectory for interest rates. This will have significant effects on the world economy as other central banks may or may not follow suit. Rising rates will also have an impact on the U.S. dollar, commodity prices, corporate earnings and the stock market. Significant emerging economies, like China, India and South Korea, have all recently cut their own interest rates to gain back the momentum they’ve lost in the last three years. This will have a counterbalancing effect on rising interest rates.

The following trends will help investors decide the best course of action as they plan for the new year.

1. Global GDP Might Break Free in the Second Half of 2016

While most analysts are obsessing over interest rates in the U.S., there is an interesting correlation being missed: interest rates and GDP growth rates of emerging economies. World GDP grew 3.8% in 2015. To put things in perspective, world GDP has grown between 3.3-3.4% from 2012 to 2014. This is far from the 5.4% growth it experienced in 2010 but is still an improvement from the flat trajectory of last three years. The same is observed in emerging economies. GDP growth rates for emerging economies have been steadily falling, from 7.5% in 2010 to 4.4% in 2014. However, 2015 seems to have broken the pattern and emerging economies rallied to grow 5% (led by India, South Korea and Malaysia).

An interesting point note in the graph below is that falling GDP growth coincides perfectly with increasing interest rates in those economies (which usually happens).

A few significant emerging economies have reduced their interest rates recently (including China, India, and Taiwan), which is likely to provide a push for global demand. World GDP growth is demand-driven by developing countries. This, along with the steadily growing growth rates of advanced economies and the euro zone, offers a ray of hope for 2016. This is reflected in the World Economic Output report published by the IMF. There is a change of GDP outlook between the two reports published in April and October (green highlighted area in the graph below).

2. Global Defense Spending Will Rise Sharply in 2016

This year has unfortunately been full of domestic and international violence. Take a look at some of these stats:

There have been more than 900 mass shootings since the beginning of 2013.

More than 1,000 people have been killed by police in the U.S. (in 2015 so far). This has resulted in a push for reforms in police action (e.g. the use of body cameras).

There was an 80% increase in terrorism deaths between 2013 and 2014. 2015 has been a particularly violent year, so the numbers might prove to be even more than 2014.

ISIS has proved to be one of the most brutal and wealthy terror groups to have challenged the world. The Western world has taken time to react to their threat, but they now control large areas of Syria and Iraq. The group reportedly brings in more than $500 million a year from oil alone. Estimates on the number of fighters have varied from 20,000 to more than 100,000. As a result, hundreds of thousands of people have been displaced from Syria and Iraq.

What does this mean for investors? Because wars in the Middle East disrupt oil supply, it might lift oil prices. Defense-related spending will go up both in the U.S. and globally. These include multiple product categories, such as tanks, navigation systems, body cameras, drones and monitoring systems.

3. Pressure on Oil Will Continue in the First Half of 2016

Oil breached the $40 per barrel mark in early December for the second time this year. There have been conflicting reports about whether or not OPEC will cut production. Supply has continued to rise even though countries are now under pressure to cut production. As per a senior OPEC delegate, Saudi Arabia will be proposing a cut of 1 million barrels per day, but it is not clear if other OPEC members will agree. As per current estimates, supply outstrips demand by more than 1 million barrels a day. It is expected that demand will be slower than usual this winter due to the El Nino effect. Even if OPEC cuts its supply, there are other drivers that are likely to pull oil prices back. If the Fed raises interest rates and the dollar continues to dominate, for example, oil prices will be under pressure. The situation, however, will change if OPEC decides to cut down supply and/or demand from emerging markets starts to pick up pace. Even if that were to happen, it will only be in the second half of 2016.

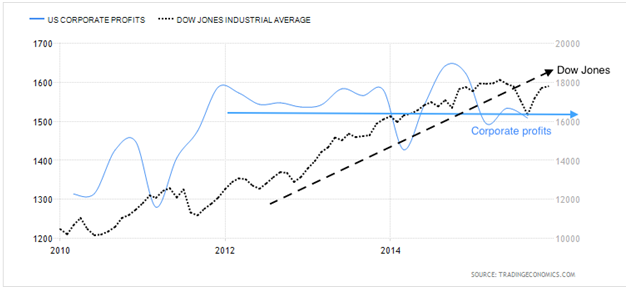

4. 2016 Might Be a Mixed Year for the Stock Markets

From the depths of the market low in early 2009, the S&P 500 has risen nearly 200%. That’s remarkable when you consider that it’s been less than six years since then. In the meantime, U.S. government debt to GDP has grown by 25%, inflation has been patchy, the GDP growth rate has been patchy, and the U.S. dollar has been rising steadily (which is not a good thing when you are coming out of a recession), and all this despite low interest rates. An even better picture is painted by the graph below. While U.S. corporate profits have been on a sideways track since 2012, the Dow Jones has had a steady upward trend. This should scare you if you are heavily invested in the stock market as it is clearly a sign of a bubble. If the stock market continue to go on a journey away from earnings, it is fair to expect a crash.

5. The Dollar Will Dominate Even More in 2016

With interest rates rising and commodity prices struggling (especially oil), the dollar is set to be even more dominant in the market. A dominant dollar certainly means that exports will be under pressure. The U.S. economic recovery, as much as the Fed would want it, can’t be export-driven if the dollar keeps rising against all major currencies. The dollar might have its own issues but other currencies have a life of their own too. For example, the yen and euro are facing downward pressure due to quantitative easing. This has, and will, keep putting more pressure on the U.S. dollar to go even higher. The Fed is worried about exports and might have started a currency war to protect its interests.

The Bottom Line

There are many anomalies to consider for 2016. There is an oil supply glut and yet no one seems to be cutting production. In the short term, oil prices will increase due to geopolitical conflicts in the Middle East.

U.S. corporate earnings have not grown as fast as the stock markets, meaning the market may need a correction to align itself to reality. Unemployment is down and there is a slight improvement in inflation and GDP growth. But an increase in interest rates might push them back. The dollar is already strong and commodity prices are in free fall. A higher interest rate is not going to help them either (of course these things can’t be decided in isolation). And yet the Fed is planning to increase interest rates this month.

All this must feel like heaven for traders and speculators because anomalies result in volatility. For investors, it is very important to keep on top of things. Maybe mutual funds are the answer? Active professional management is beneficial in uncertain times.

For more frequent updates follow me @tanmoyroy.

Sign up for Advisor Access

Receive email updates about best performers, news, CE accredited webcasts and more.

The phrase ‘bear market’ has been thrown around a lot lately, but it...

Advertisement

×

Wait! Do you know all the important aspects of mutual funds?

×

Free Advisor Access newsletter emailed to you.

Receive free and exclusive email updates for financial advisors about best performers, news, CE accredited webcasts and more.

Sign up for Advisor Access

Receive email updates about best performers, news, CE accredited webcasts and more.

Disclaimer: By registering, you agree to share your data with MutualFunds.com and opt-in to receiving occasional communications about projects and events. The contents of this form are subject to the MutualFunds.com

Privacy Policy.

You can unsubscribe at any time.