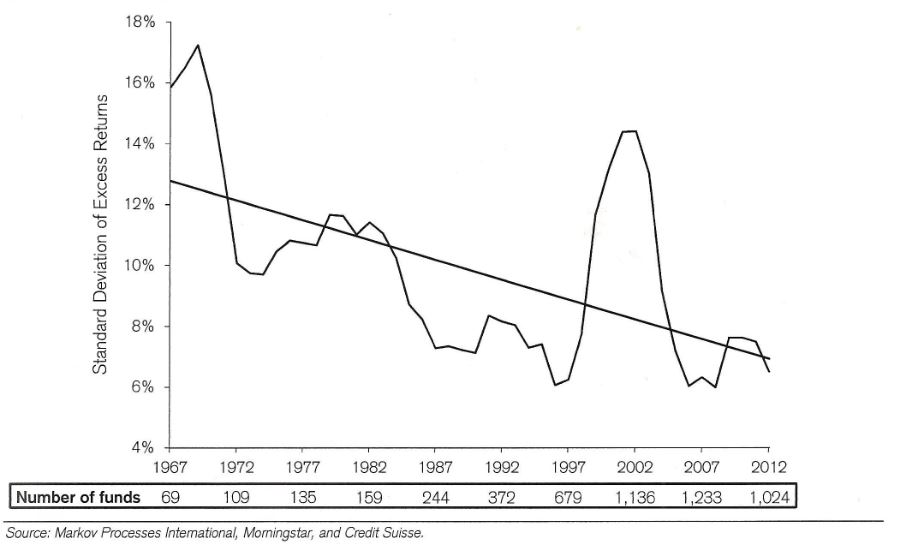

The study Conviction in Equity Investing by Mike Sebastian and Sudhakar Attaluri, which appeared in the summer 2014 issue of The Journal of Portfolio Management, provides further evidence of a declining ability to generate alpha. They found that:

- Since 1989, the percentage of mutual fund managers who evidenced enough skill to basically match their costs (i.e., showed no net alpha) has ranged from about 70% to as high as about 90%, and by 2011 it was at about 82%.

- The percentage of unskilled managers has ranged from about 10% to about 20%, and by 2011 it was at about 16%.

- The percentage of skilled managers began the period at about 10%, rose to as high as about 20% in 1993, and by 2011 fell to just 1.6%.

Lubos Pastor, Robert Stambaugh, and Lucian Taylor, authors of the August 2013 paper Scale and Skill in Active Management, provide further insight into why the hurdles associated with generating alpha are getting higher. The authors, whose study covered the period from 1979 to 2011 and more than 3,000 mutual funds, concluded that fund managers have become more skillful over time.

They write, “We find that the average fund’s skill has increased substantially over time, from -5 basis points (bp) per month in 1979 to +13 bp per month in 2011.” However, they also found that the higher skill level has not translated into better performance. They reconcile the upward trend in skill with no trend in performance by noting, “Growing industry size makes it harder for fund managers to outperform despite their improving skill. The active management industry today is bigger and more competitive than it was 30 years ago, so it takes more skill just to keep up with the rest of the pack.” These findings are consistent with everything we have discussed so far.

Pastor, Stambaugh, and Taylor also came to another interesting conclusion: the rising skill level they observed was not due to increasing skill within firms. Instead, they found that “the new funds entering the industry are more skilled, on average, than the existing funds. Consistent with this interpretation, we find that younger funds outperform older funds in a typical month.”

For example, the authors found that “funds aged up to three years outperform those aged more than 10 years by a statistically significant 0.9% per year.” Consistent with Ellis, the authors hypothesized that this is the result of newer funds that have managers who are better educated or better acquainted with new technology (though they provide no evidence to support that thesis). They also found that all fund performance deteriorates with age, as industry growth creates decreasing returns to scale, and newer and more skilled funds create more competition.