Income is certainly plentiful in the high-yield bond space. After last year’s drubbing and the Fed’s path of rate hikes, junk bonds are now yielding close to 10%. For many advisors and investors, those high yields are too tantalizing to pass up. Flows into high-yield bond vehicles have surged in recent months.

However, investors and advisors may want to change their tune when it comes to which products they’re putting their money into.

With default rates rising and the economy getting dicey, active management could be the savior in the space. With the number of active junk bond ETFs growing, investors have plenty of opportunity to reduce their risk while still getting some hefty yields.

Bond Yields & Defaults Rise

Like much of the fixed income market, high-yield bonds were hit hard as the Fed raised rates. Doubly in fact. High-yield bonds are those issued by firms with less than investment-grade credit ratings. Typically, junk bonds are rated BB+ or lower by Standard & Poor’s and Ba1 or lower by Moody’s. Because of the default potential, investors want to be compensated for owning them. So, they offer higher yields than say a 10-year Treasury bond.

As the Fed raised rates, the sector was hit with a double whammy. New junk debt coming to market reflects the higher rates, while the economic effects of the higher rates, i.e., recession potential, grows – both send investors out of junk and into safer pastures. This helps explain why the ICE BofA US High Yield Index is currently yielding over 8%.

That’s a juicy yield and closer to the sector’s historical average. The thing to remember is that they don’t call them junk for nothing.

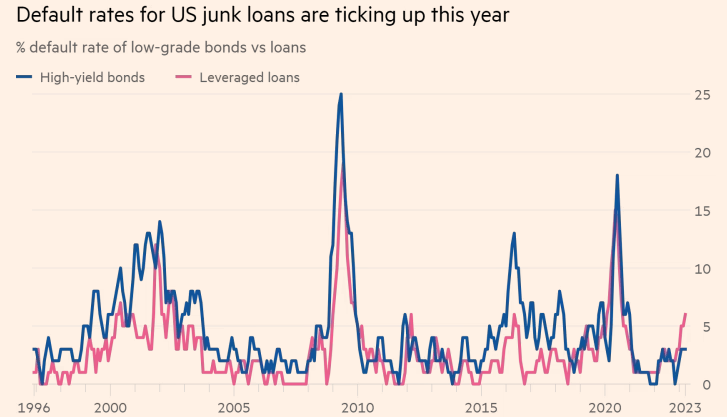

This is playing out today. Thanks to falling revenues and higher interest expenses, default rates for high-yield bonds are starting to grow. According to Goldman Sachs, there have been 18 debt defaults, totaling over $21 billion, from the beginning of the year til the end of May. That’s higher than the number of defaults in 2021 and 2022 in both number and dollar value of bonds. 1

This chart from the Financial Times shows the current tick upward in both high-yield bonds and leverage loans (junk’s floating rate sister) default rates.

Source: FT.com

Both ratings agencies Fitch and S&P Global now predict that default rates will rise above historic levels by the end of the year.

Active Management Can Lower Risk

For investors, it’s a Catch-22. With yields so high, junk bonds are still a great way to add an income boost to a portfolio. However, risks of default are growing. Balancing the two could come down to active management and ETFs. It turns out that high-yield bonds are a wonderful place for investors for active management to prove its worth.

For starters, active managers don’t have to stick to the index, which is particularly important in the high-yield space. Bond indexes are generally weighted based on the amount of debt outstanding. Firms with the most debt get a higher place in the index. With this, you’re basically rewarding the biggest debtors with more pull on the index. That’s an issue when defaults start to happen.

Secondly, active managers are able to conduct credit and cash flow research into the underlying firms. This allows them to avoid pitfalls and defaults before they happen. Moreover, they can buy bonds at discounts to their value to provide a larger safety and, perhaps, increased yields.

It turns out, it works. According to Morningstar, over the last 10 years, 76.9% of the lowest-cost active high-yield funds managed to beat their passive rivals. Looking at the entire sector, 56% of active managers beat their passive benchmarks.

Due to their structure, ETFs are less expensive to operate and many firms pass on the savings to investors. Meanwhile, the creation-redemption mechanism allows for investors to realize tax savings. This makes it ideal for the high-yield market.

Getting Active With Your High-Yield Exposure

Given the rising default risk and active management’s ability to achieve excess returns while reducing risk in the fixed income type, investors may want to get active with their junk bonds. The win is that there are numerous ETFs on the market targeting the space.

With over $1.54 billion in assets, the First Trust Tactical High Yield ETF is the largest and oldest fund in the active space. Featuring a concentrated portfolio, the ETF yields a strong 7.99%. Another top choice could be the SPDR Blackstone High Income ETF. Blackstone is one of the largest alternative managers in the world and features a deep credit research bench. These two funds currently garner the bulk of the assets in the space.

However, new active high-yield ETFs from a wide range of issuers, such as T. Rowe Price, Franklin Templeton, PGIM and Principal, have all launched within the last couple of quarters. It’s only a matter of time before they gather serious assets and trading volumes.

Active High Yield ETFs

| Ticker | Name | AUM | YTD Price Ret (%) | Exp Ratio | Yield | Actively Managed? |

|---|---|---|---|---|---|---|

| FLHY | Franklin High Yield Corporate ETF | $214.5M | 3.4% | 0.4% | 6.1% | Yes |

| YLD | Principal Active High Yield ETF | $105.1M | 3% | 0.41% | 6.8% | Yes |

| PHYL | PGIM Active High Yield Bond ETF | $93.3M | 1.5% | 0.53% | 6.5% | Yes |

| HYBL | Spdr Blackstone High Income ETF | $125.7M | 1.4% | 0.70% | 7.8% | Yes |

| THYF | T Rowe Price US High Yield ETF | $22.7M | 1.4% | 0.56% | 8.6% | Yes |

| HYFI | AB High Yield ETF | $67.5M | 1.1% | 0.60% | 6.7% | Yes |

| SIHY | Harbor Scientific Alpha High-Yield ETF | $114.1M | 1.3% | 0.48% | 7.8% | Yes |

| HYLS | First Trust Tactical High Yield ETF | $1.546B | 0.8% | 0.95% | 6.3% | Yes |

It’s also a matter of time before other big bond shops and ETF issuers launch their own active junk bond ETFs. Ultimately, this one area where active management can make a huge difference in returns and risk control.

The Bottom Line

Junk bonds are currently yielding 8% to 10%. This fact has drawn many investors and financial advisors into the sector looking for income, which could be a problem as there is still plenty of risk to be had. Default rates for the sector are starting to rise. Here, active ETFs can help mitigate the risks and improve returns. Investors looking for high income should turn to the products.

1 FT.com (June 2023). US junk loan defaults surge as higher interest rates start to bite