If you’re shopping for a mutual fund, it’s not surprising to find yourself intimidated by the sheer variety of offerings readily available at your fingertips. With well over 7,000 equity-focused funds to pick from, some investors are bound to get lost as they look for a product that best aligns with their long-term goals and risk preferences.

Luckily, we’re here to offer you a straightforward guide that helps to combat much of the confusion that is all too often associated with buying a mutual fund. The seven questions below are aimed at simplifying the screening and selection process and should help steer you on a path towards finding the investment vehicle best suited for you.

1. What is your goal?

The first and most important question, and one that is frequently overlooked, has more to do with you than the list of mutual funds offered for purchase through your broker. The mutual fund buying process should start with the investor addressing his or her goals; this includes answering questions about your investment objectives, risk-preference, and time horizon.

For starters, ask yourself what your objectives are. As straightforward as this may seem, you would be surprised how many investors end up buying into products that don’t truly align with their own goals to begin with. To make things easier, your investing objective should more or less fall into one of these three categories:

Growth – This sort of strategy aligns with younger and more risk-tolerant investors whose top priority is to increase the value of their investments over time.

Capital Preservation – This sort of strategy aligns with more conservative investors and perhaps those nearing retirement whose top priority is to safeguard their assets and ensure stability in the portfolio.

Income – This sort of strategy aligns with yield-starved investors and retirees whose top priority is to generate a meaningful current income stream from their portfolio.

Because no single investment vehicle can realistically address all three of these objectives in a balanced manner, it’s important that you first determine what approach is best for you before moving onto compare different mutual funds.

2. What does the fund hold?

Now that you’ve determined your investing goals, it’s time to look under the hood and make sure that a fund’s underlying portfolio actually aligns with your desired objective. The reason you need to dig deeper and look through a fund’s portfolio yourself is because you can’t actually tell what it holds just by looking at the name; furthermore, a fund’s name can at times be altogether misleading, further warranting a good look under the hood.

Let’s suppose you have a growth objective in mind and you’ve narrowed down your list of choices to a number of funds targeting large-cap equities. You might think you’re all set, and now it’s just a matter of picking the cheapest one that also has a decent manager. Well actually, you’re not quite there yet. Even among mutual funds that fall under the same umbrella, there are meaningful differences to take into consideration.

Within the large cap universe alone there is an unbelievable variety of potential investments; for example, one fund might focus exclusively on U.S.-based companies while another might include securities from developed and emerging markets. Furthermore, one fund might be tilted towards a particular sector or a group of stocks, while another one might not follow a traditional market capitalization-weighted index at all.

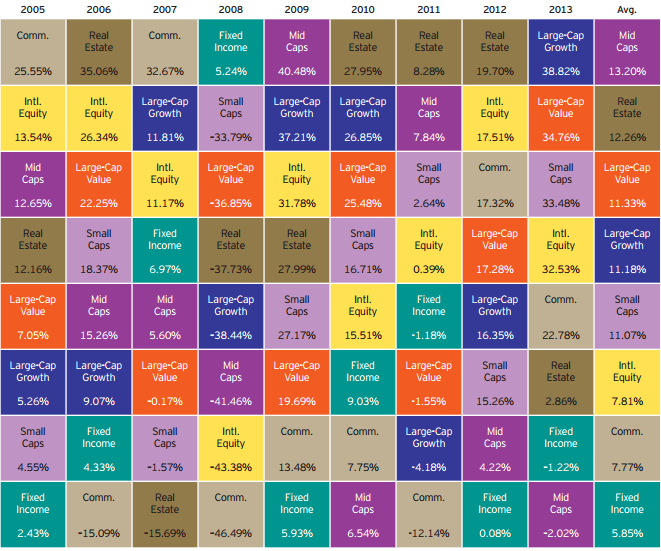

Consider the historical returns table below compiled by Invesco:

The important takeaway here is to note the sheer diversity in returns over the years across seemingly similar asset classes. For example, notice how in 2009, Large-Cap Growth turned in a gain of 37%, while Large-Cap Value was up only 19%. This is a major difference in returns between two asset classes that many assume to be one and the same.

The lesson here is to take a look under the hood of a mutual fund because its name and category don’t necessarily reveal what types of securities the fund actually invests in.

3. How expensive is it?

Picking a fund whose underlying holdings best align with your objectives is critical; the next step is keeping expenses to a minimum. Whether you choose to think of it this way or not, the fact of the matter is that every dollar spent to cover you fund’s management fee is a dollar less contributing to your own return. Over a long enough time horizon, seemingly small differences in expense fees can add up and make a big difference in your portfolio.

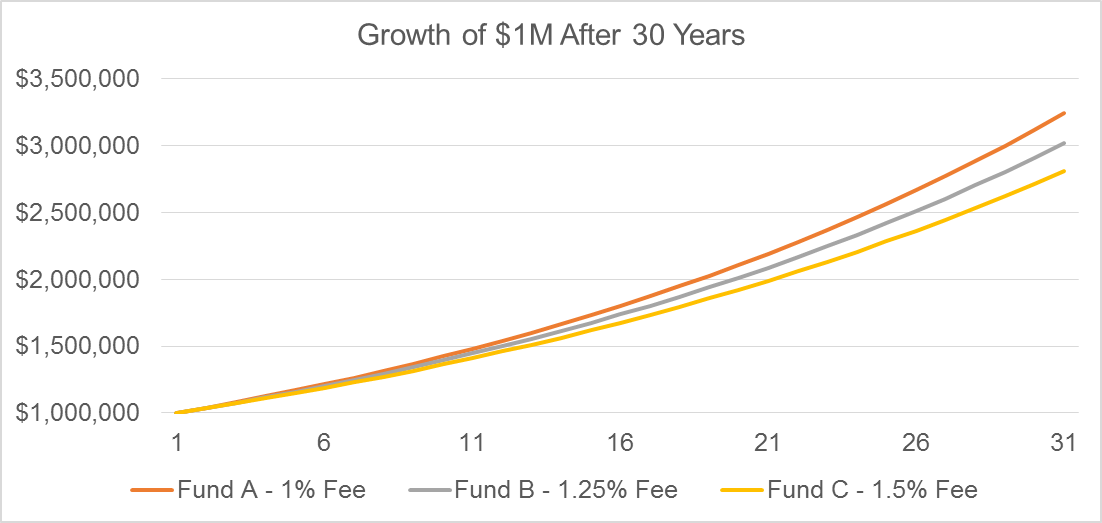

Consider the graph below, which illustrates the growth of $1,000,000 over 30 years assuming an annual return rate of 5% across three hypothetical funds, each with a slightly different expense ratio:

The important takeaway here is to note the ending values of the three hypothetical portfolios; the cheapest one, Fund A, leaves you with $3,243,398 after 30 years while the more expensive counterpart, Fund C, leaves you with $2,806,794. Though this is an overly simplified investing example, the power of compounding returns is nonetheless illustrated, showcasing the impact of a small difference in fees over the long-haul.

The lesson here is to take the time and do your homework when picking a mutual fund; after you’ve narrowed down your objective and desired holdings, you need to compare the costs of all the available options and go with the fund that best aligns with your goals while keeping expenses as low as possible.

4. Who runs the fund?

Now that you’ve narrowed down your list of potential investments to a handful of funds, it’s time to consider who’s in the driver’s seat of each vehicle. Much of a mutual fund’s success can depend on the skill of the portfolio manager in charge.

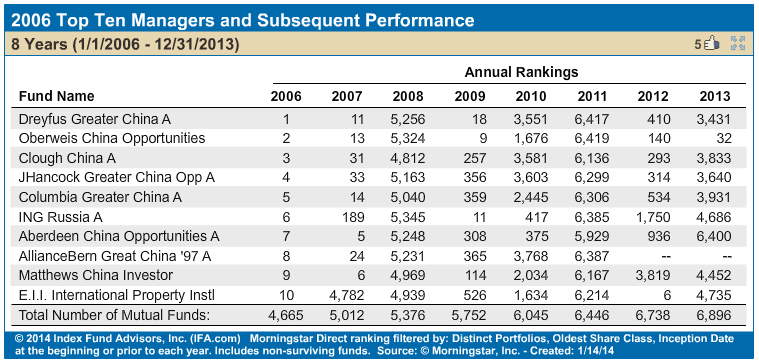

Consider the table below, which showcases the top ranked mutual funds in 2006, and their subsequent rankings in the years following:

The biggest takeaway here is that an overwhelming majority of the top ranked funds in one year failed to make the top-10 rankings in the years following. This sort of inconsistency in returns is the reason why investors should take the time to ask who’s running their fund and, more importantly, dig deeper and investigate that particular manager’s track record over the long-haul.

It’s true that past performance is no guarantee of future returns. This is why investors are better off going with a manager that boasts a solid 15-year track record, instead of one that had an absolutely stellar run one year and completely flopped the next.

5. What’s in the fine print?

Taking the time to read through a fund’s prospectus can be an eye opening, albeit not a very exciting, experience. Upon closer examination of the fine print, some might be caught off guard by the various fees disclosed. Remember our previous example that illustrated the power of compounding returns when costs are minimized? Well, that’s why it’s important to be aware of the different expenses associated with owning a funding, including:

Front-End Load – This is a commission or sales fee that you pay upon making the initial investment. For example, if you invest $100,000 in a mutual fund with a 2% front-end load, you will end up paying $2,000 in fees, leaving you with a $98,000 investment.

Back-End Load – This is a commission or sales fee that is incurred upon the sale of your investment. For the most part, this type of fee is associated with Class B shares (read more about this below).

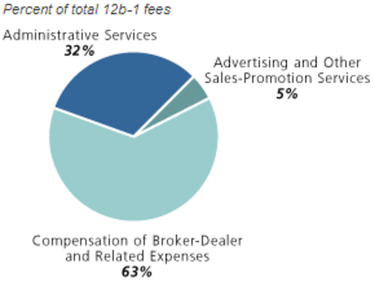

12b-1 – This is an ongoing fee that is part of a fund’s expense ratio; it’s used to pay for brokerage expenses as well as advertising and marketing costs, making the funds that boast this fee less than ideal choices for cost-conscious investors. Consider the pie chart below, which illustrates the breakdown of the much-debated 12b-1 fee:

Keeping your costs low is a surefire way to improve your returns right off the bat, which is why taking the extra time to read the fine print is so important.

6. Is it tax-efficient?

It’s without a doubt that taxes will take a bite out of your investment, which is why opting for a more tax-efficient fund is another surefire way to boost your returns over time. So, what exactly makes one fund more tax-efficient than another?

Methodology – The investment approach utilized by a particular fund plays a key role in shaping its tax-efficiency; for the most part, index-based funds are more efficient than their actively-managed counterparts.

Turnover Rate – This refers to the fund’s trading frequency, which relates largely to its methodology.

Distributions – The amount and type of distribution paid out affect the tax-efficiency of a fund.

By opting for a more tax-efficient fund after doing your homework, you’ll effectively keep more of what you earn over time.

7. Which share class is right for me?

After you’ve settled on a fund, you need to ask yourself which share class is right for you? Mutual funds come in three classes, A shares, B shares, and C shares – each one is essentially the same portfolio of securities, and the only difference between them is the type of fees and expenses associated with them. For the most part, Class A shares bear front-end load charges, Class B have back-end charges, while Class C might evade load charges altogether at the cost of a higher expense ratio.

Take the time to read through and understand the various fees and nuances associated with each class of shares for a particular fund and select the one that best aligns with your objectives.

The Bottom Line

Shopping around for a mutual fund can be a tall order when you consider the sheer number of offerings and the quirks and nuances associated with each one. Investors can simplify this intimidating process by first determining their own objectives and risk preferences; next, it’s important to consider the finer details, such as the underlying holdings and additional fees. All in all, investors stand to make more savvy financial decisions after taking the time to get educated and doing some good ole fashioned research.