Let’s look at the evolution of actively-managed ETFs and how the different types impact investors.

See our Active ETFs Channel to learn more about this investment vehicle and its suitability for your portfolio.

A Brief History

Until recently, active ETFs had to disclose their holdings every day. While that’s not a problem for passive funds mimicking a public index, it’s a potential drag on alpha generation capability for many mutual fund managers. So, in 2020, the SEC approved the first semi-transparent ETFs, enabling managers to publish a proxy index or involve a third party.

Under today’s rules, semi-transparent ETFs can only provide exposure to long-only U.S.-listed equities and derivatives. However, the SEC may permit non-U.S. equity, fixed income, and additional types of derivatives in the future. Regulators are likely waiting for managers to build a track record and prove secondary market spreads and liquidity are adequate.

Despite these limitations, active semi-transparent ETFs have grown from about $100 billion in assets to over $300 billion, according to NYSE data released in February 2022.

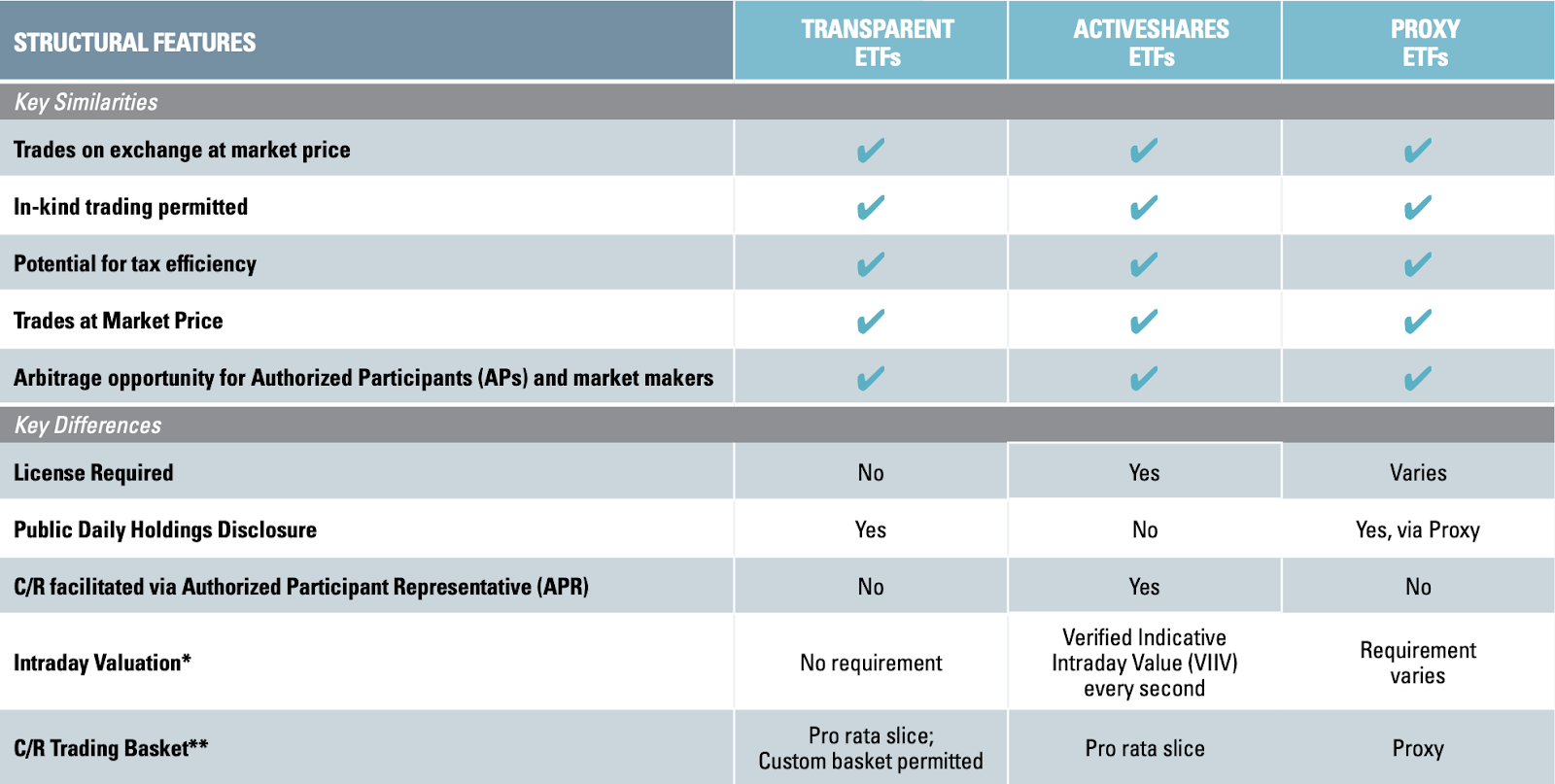

Types of Active ETFs

- Transparent

- ActiveShares

- Proxy

While every structure trades at a market price and offers the same tax efficiency, they have varying levels of public disclosure, intraday valuation techniques, and license requirements (see chart shown below for details). And, as we mentioned earlier, semi-transparent funds have asset limitations.

Source: Brown Brothers Harriman & Co.

Transparent ETFs

Transparent ETFs are the most common type of active ETF. They rely on publicly disclosed daily portfolio holdings to facilitate market trading and creation/redemption (C/R) activity. Unlike ActiveShares or proxy ETFs, they can also leverage pro-rata or custom baskets based on their fund holdings to achieve maximum tax efficiency and flexibility.

Since they disclose holdings daily, these ETFs provide investors with the most transparency and liquidity. For example, full daily disclosure helps keep secondary market spreads tight because market makers can efficiently hedge. And investors can view the stocks they own at any time to understand how the ETF fits within their portfolio.

ActiveShares ETFs

ActiveShares ETFs provide daily portfolio disclosures to an Authorized Participant Representative (APR) that confidentially facilitates market trading and C/R activity. Under the SEC’s rules, these structures require calculating a verified intraday indicative value (VIIV) every second and quarterly or monthly portfolio disclosures.

While the lack of daily disclosures could increase spreads, early data suggests that they trade similarly to their fully transparent counterparts. That said, they are limited to U.S.-listed long-only equities, which could be a deal-breaker for fixed income or other allocations. And they have less flexibility when it comes to creating C/R baskets.

Proxy ETFs

Proxy ETFs publicly disclose a daily proxy portfolio, or tracker basket, that mimics the intraday return of the actual portfolio to facilitate trading and C/R activity. Like the ActiveShares ETFs, issuers must disclose the actual portfolio holdings on a quarterly or monthly basis. These structures are common with Fidelity, T. Rowe Price, Invesco, and others.

Like ActiveShares, proxy ETFs are limited to U.S.-only long equities and could face higher spreads (although data suggests otherwise). They also have less flexibility when it comes to creating C/R baskets.

The Bottom Line

That said, emerging data suggest that ActiveShares and proxy ETFs trade similarly to fully transparent ETFs. These data could help encourage the SEC to close the gaps between the two fund types in the future.

Take a look at our recently launched Model Portfolios to see how you can rebalance your portfolio.