While municipal bonds have grown in popularity, they are still ignored by the bulk of the investing public. Often seen as an asset class for the very rich, many investors don’t understand muni bonds and what they can do for their portfolios. Several myths about the asset class remain, which prevent investors from understanding the benefits of using them in their portfolios – no matter what tax bracket they are in.

Luckily, asset manager Goldman Sachs sheds some light on these myths. By uncovering the truth, investors should want to take up the muni bond mantle and buy the bonds for their income needs.

A Brief Overview

The fixed-income world is vast, with a wide variety of IOUs out there. Muni bonds are just one such security. Munis are issued by state and local governments to fund their budget needs, launch special projects, like a new park or police station, or pre-fund future revenue sources.

Munis have existed for a long time, but they started to come into their own back in 1913. It was then that President Wilson signed the 16

However, because of the tax-free nature of their coupon payments, many investors often think of muni bonds as a tool for the very rich to lower their taxes. This is just one of the myths that surround municipal debt.

Goldman Sachs Breaks Down Munis

The truth is that no matter the tax bracket, investors can gain from adding muni bonds to their portfolios. According to the Goldman Sachs white paper on many of the inaccurate themes facing Muni bonds, four main muni bond myths need busting. Understanding how muni bonds function can allow more investors to take the plunge and see how the bonds can truly perform in their portfolios. 1

Myth 1: Municipal Credit Risk is Similar to Corporate Credit Risk

Credit risk affects all bonds, and municipalities are no different. However, many investors wrongly believe that muni bonds are riskier than they are. U.S. Treasury bonds are considered the gold standard, because Uncle Sam can, in theory, raise taxes as much as the Federal government likes to pay off debts.

Local and state governments, like those in Texas or Racine, Wisconsin, can only raise their taxes to a certain point before people start moving to areas with lower taxes. This means there’s a cap on how much cash flow local and state governments can generate to repay their muni debt obligations, making these bonds riskier than U.S. treasury bonds, which have more flexibility as the Federal government can have more sources to raise funds. However, many investors still incorrectly lump muni bonds with investment-grade corporate bonds when it comes to risk profiles.

According to Goldman Sachs, this is wrong.

Thanks to diverse revenue sources and taxing ability, muni bonds are far less risky than corporate bonds. The evidence shows up in their historic default rate vs. corporate bonds: Looking at the average 10-year cumulative default from 1970-2021 for muni bonds, it was just 0.15%, compared to 10.36% for corporate bonds. Looking at strictly investment-grade categories for both, the rates are 0.09% and 2.17%, respectively.

Myth 2: Muni Bond Returns Are Not Consistent

The muni bonds sector tends to be boring. So, when they have a bad year or a major event, they tend to make headlines. This has perpetuated the myth that muni bond returns are not steady or that the returns are not consistent.

The opposite is true.

Muni bonds are some of the steadiest asset classes out there. Thanks to the widespread buy & hold investor base, muni bonds hardly ever see negative returns. Goldman reports that since 1980, over rolling 3-year periods, investment-grade muni bonds have only experienced negative returns just 2% of the time.

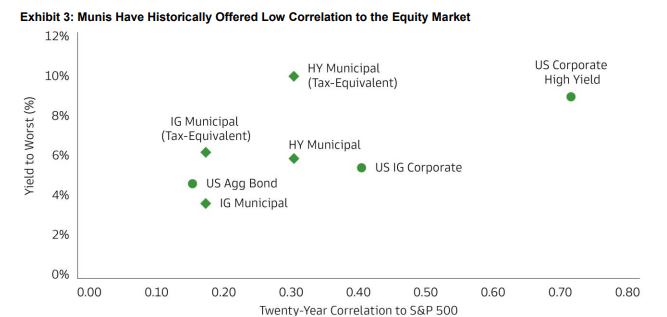

Myth 3: High-Yield Muni Bonds Are High-Risk Investments

Like corporate bonds, muni bonds can have a varied degree of credit ratings, including high-yield muni bonds. For many investors, they equate these high-yield muni bonds with high-yield junk bonds. But, despite the names and bigger yields, there are stark differences.

Thanks to the lower default rates, high-yield muni bonds function differently and have lower volatility than junk bonds. Moreover, this chart from Goldman Sachs shows that high-yield muni bonds have had a much lower correlation to the stock market than junk bonds, enabling them to be better portfolio diversifiers.

Source: Goldman Sachs

Muni Myth 4: The Universe of Muni Bonds is Limited

Most investors think of muni bonds as a “category” investment, sort of like emerging markets. Allocations are painted with a broad brush stroke. But, just as China and Romania are completely different nations, so is one state vs. another.

The muni bond market is very diverse, with over 50,000 different issuers in the U.S. To put that into context, there are only about 3,700 publicly listed stocks, highlighting a much bigger opportunity set for the muni market.

Adding Some Muni Muscle

Given that muni bonds are perhaps a better deal than many investors perceive, adding them to a portfolio certainly makes sense. According to Goldman Sachs, muni bonds offer wonderful current yields as well as plenty of strong risk-adjusted returns compared to other asset classes.

Luckily, muni bonds can be quickly added via ETFs for a low cost. Given the huge diverse nature of the sector (busted Myth 4 mentioned previously), buying individual muni bonds can be a tough nut to crack, which lends itself to active management. This busts another myth that active underperforms passive. When it comes to municipal bonds, the opposite is true, with many active managers beating their benchmarks in the sector.

Municipal Bond Funds

These mutual funds and ETFs were selected based on their YTD total return, which ranges from -0.1% to 2.3%. They have expenses between 0.05% to 1.02% and assets under management between $45M to $35B. They are yielding between 2.8% and 4.2%.

| Ticker | Name | AUM | YTD Total Ret (%) | Yield (%) | Exp Ratio | Security Type | Actively Managed? |

|---|---|---|---|---|---|---|---|

| PTHAX | Putnam Tax-Free High Yield Fund | $632M | 2.3% | 3.7% | 1.02% | MF | Yes |

| HYMB | SPDR® Nuveen Bloomberg High Yield Municipal Bond ETF | $1.9B | 2.2% | 4.2% | 0.35% | ETF | No |

| MDYHX | BlackRock HY Municipal Fund USD Class A | $2.15B | 1.9% | 3.9% | 0.85% | MF | Yes |

| FLMI | Franklin Dynamic Municipal Bond ETF | $126M | 1.8% | 3.6% | 0.30% | ETF | Yes |

| MEAR | BlackRock Short Maturity Municipal Bond ETF | $615M | 0.7% | 3.3% | 0.25% | ETF | Yes |

| PVI | Invesco VRDO Tax-Free ETF | $45M | 0.6% | 2.8% | 0.25% | ETF | No |

| MUNI | PIMCO Intermediate Municipal Bond Active ETF | $1B | 0.2% | 3.4% | 0.35% | ETF | Yes |

| JMUB | JPMorgan Municipal ETF | $725M | 0.2% | 3.5% | 0.18% | ETF | Yes |

| MUB | iShares National Muni Bond ETF | $34.3B | 0.1% | 3.0% | 0.05% | ETF | No |

| TFI | SPDR Nuveen Bloomberg Municipal Bond ETF | $3.24B | -0.1% | 2.9% | 0.23% | ETF | No |

In the end, investors have some common misconceptions about municipal bonds. Those misgivings have them ignoring the sector in spades. However, the truth is, that muni bonds make for a wonderful asset class for a lot of portfolios. Taking the time to understand the sector and adding it to a portfolio could be wonderful for income and returns.

The Bottom Line

Thanks to their tax-free nature, many investors ignore muni bonds, creating plenty of misconceptions about the asset class. However, Goldman Sachs busts these myths, aimed at helping investors improve their understanding of the asset class and incorporate it in a better way in their portfolios.

1 Goldman Sachs (June 2023). Busting Myths About Munis