America continues to face a retirement crisis. And the statistics are downright scary. The vast bulk of Americans haven’t saved enough for their golden years. The rise of self-funding via 401ks and the dwindling of pension benefits has continued to exacerbate the problems. To that end, a variety of policymakers and pundits have tried to come up with solutions to the major issue.

The answer may be as simple as giving kids some cash and letting the magic of compounding work its charm.

A variety of proposals now exist that would provide young children with investment accounts designed to let them accumulate retirement savings for later in life. And this just might be the answer we need to tackle the retirement crisis head on.

Scary Stats

America’s state of retirement is facing a crisis and it doesn’t seem to be getting any better in the near term. The statistics all around are downright scary. The creation of self-funding vehicles like 401ks and 403bs has shifted the burden of saving for our golden years from corporations via pensions to individuals. In that, Americans just aren’t doing a good enough job.

The pressures of everyday life have many Americans inadequately prepared for retirement. According to a 2017 report from the Government Accountability Office (GAO), for Americans between the ages of 55 and 64, the median retirement savings amount was just over $107,000. According to the GAO, this amount of money translates to just a $310 monthly payment when annuitized. The discrepancy between high income workers and lower income workers is vast within that data, with many Americans on the lower income scale having no savings at all.

Moreover, while both versions of the SECURE Act are designed to help more workers save for retirement, there’s still more than 30% of all American workers who don’t have access to a workplace retirement plan.

Adding in pressures to safety nets like Social Security, which is only guaranteed till 2035, increasing longevity, and the growing problem of forced early retirement, Americans are truly facing dark times ahead.

The Magic of Compounding

Albert Einstein called compound interest “the eighth wonder of the world.” Time plus a steady rate of return can create vast wealth. This fact is the basis behind a series of new proposals, legislation, and other policy points. They all have the same basic premise: give children a little bit of money today and let time and market returns do their job.

So-called State-Sponsored Child Investment Accounts (SCIAs) were originally proposed for college education and the reduction of student loan debt. Fourteen states have set up SCIAs for students. For example, Maine provides automatic enrollment and $500 toward future college education for every baby born in the state. Pennsylvania offers $100 deposited into a 529 plan. So far, these programs have proven to be successful in helping make college more affordable, particularly for lower income families.

This is where the idea for using SCIAs for retirement savings was formed. The idea is simple. Giving babies money, investing it in the market, and letting it grow till retirement provides a low initial-cost solution and gives retirement security later in life.

Two major hedge fund managers have brought the bipartisan effort to the forefront.

Back in December 2020, Pershing Square’s Bill Ackman came up with a proposal of a ‘Birthright fund.’ Each child born in the U.S. would have a fund seeded with $6,750 at birth. These funds would be invested in a series of low-cost index funds. Individuals would be prohibited from accessing and withdrawing the funds until at least age 65. According to Ackman and using historical market returns of 8%, that amount of money would grow to $1 million by age 65. Ackman’s plan would cost the U.S. government just $26 billion per year based on current birth rates. 1

Source: New York Times DealBook Newsletter

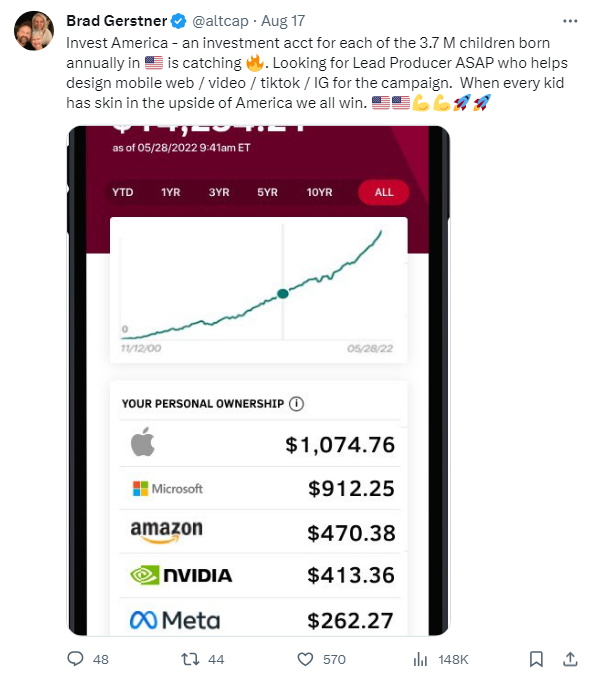

Similarly, Bard Gerstner, CEO and founder of Altimeter Capital, combines both government and free enterprise help. Under Invest America, Gerstner’s plan would start with a $1,000 seed from the federal government. Parents would be able to make contributions to their children’s accounts. The kicker is that corporations would be able to make matching contributions. Speaking at CNBC’s Delivering Alpha summit, Gerstner envisions Invest America as “401ks from birth, where corporations like Uber or United will then match those grants to those kids at birth.” 2

Source: X, formerly known as Twitter

Both proposals aren’t without their critics. Pundits have worried about these types of plans circumventing and undermining Social Security. At the same time, market risk is now on the table. A few years of lower-than-expected returns could place today’s children in a precarious boat, whereas Social Security is designed to be a ‘guaranteed asset’. Moreover, some pundits have expressed concerns about the private matching grants and the requirements that parents contribute to the accounts to get these grants. There are already plenty of ways for parents to help their kids save and those that take advantage are often of higher income. The private/public fund may not achieve its goal of reducing wealth inequality as intended, but perhaps exacerbate it.

However, Invest America points out that even without additional money, the initial $1,000 would grow to more than $107,000 by age 67 at a 7% growth rate. If that investor started at 20, that portfolio would only grow to $26,000. That’s a meaningful addition to a retirement balance.

A Smart Start

Both the current proposals follow a long history of similar, Congress-sponsored ideas. For example, 2009’s America Saving for Personal Investment, Retirement, and Education (ASPIRE) Act provided each child born after 2010 with $500 to be invested in a series of broad index funds. The government provided matching grants to parents based on income requirements, with some tiers receiving free yearly contributions. The US-Accounts: Investing in America’s Future Act provided a similar structure. Rather than just be for retirement, the bill could be used for items such as home ownership and medical care. Both bills featured strong bipartisan support, only to never advance past committee stages.

So, proposals like Ackman’s and Gerstner’s have some precedent and an uphill battle to fight.

Ultimately, these proposals and other State-Sponsored or Federal-Sponsored Child Investment Accounts serve to use the magic of compounding to create retirement savings. That’s a wonderful thing given the issues and lack of retirement preparedness that many Americans are facing. It will be interesting to see if Ackman’s, Gerstner’s or other proposals will ever make it out of committee and to a vote.

As we wait, parents have some ability to invest for their children. Custodial and UGMA/UTMA accounts have existed for years. Meanwhile, the new SECURE Act includes provisions that allow parents to convert some 529 plan savings into a Roth IRA, which could provide some savers with a leg up on their children’s retirement savings.

However, none of these do anything to deal with wealth inequality. That will take some serious muscle.

The Bottom Line

Many Americans are facing a retirement crisis. But hope could be on the way. New proposals from two hedge fund greats use the magic of compounding to turn small sums into large balances by retirement age. Given the issues facing savers, they are getting a hard look from pundits and policymakers alike.

1 Forbes (Dec 2020). Bill Ackman: Give Every Child $6,750 So They Retire As Millionaires

2 CNBC (Sep 2023). Delivering Alpha Recap