Investors in retirement face a unique problem. How do they turn their hard-earned savings into a paycheck that will last them for their entire lifetimes? And there are many ways pundits, financial planners, and gurus suggest doing just that. But according to asset manager BlackRock, much of that advice may be wrong.

Investors need to have an income-centric focus.

It turns out that focusing on income first through a multi-asset approach can lead to better results, reduce volatility, and extend the life of a portfolio. For investors, it’s a departure from some common advice.

A Two-Pronged Approach

When most investors build a portfolio, they often use a mix of stocks and bonds. This is the basis for modern portfolio theory. The idea is that the combination of these two asset classes creates lower volatility; when combined, they smooth each other out. If stocks are down, bonds pick up the slack, and vice versa. This creates consistently positive long-term returns.

However, according to a new white paper by giant asset manager BlackRock, we’ve been doing this all wrong. Instead of focusing on stocks and bonds at the same time, we should be focusing on them one right after the other.

BlackRock summarizes that there are two phases to retirement: accumulation and decumulation.

In accumulation, it’s about saving for retirement. But rather than owning stocks and bonds or shifting from a high concentration of stocks to bonds as we age, investors should stick to just equities and let time weather the storm.

Data underscores this reasoning. Suppose a hypothetical investor puts $100,000 into the S&P 500 at the start of the year 2000. Each year, he contributes an inflation-adjusted $4,000 to his savings. Even accounting for the tech bubble, the Great Recession, and the pandemic, this investor would have more money than a similar investor choosing a 60/40 balanced portfolio or one that became more conservative as they aged. We’re talking an ending portfolio balance of $772,000 versus $617,000 and $590,000, respectively.

Ultimately, time in the market heals all wounds and the growth of the stock market wins out.

Decumulation Equals Income

After we’ve saved it, we need to spend it. This prong of retirement is called decumulation. And here again, BlackRock’s advice goes against the grain. Normally, investors will use a combination of fixed income investments and asset sales to generate required spending needs. But BlackRock says this is wrong. Investors should be focusing on income first.

Again, the data provides the proof.

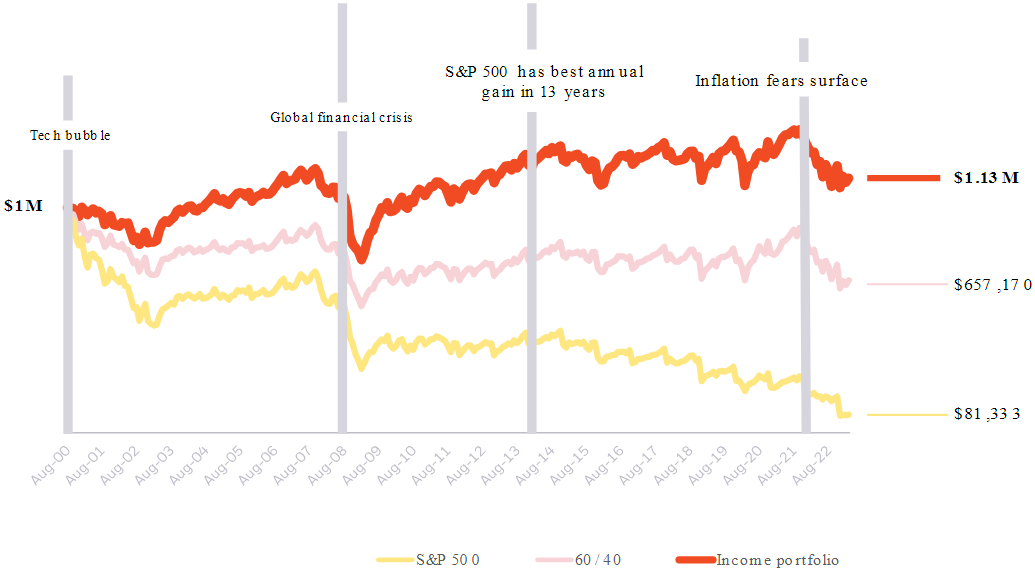

An investor has $1 million saved and a $40,000 annual portfolio income need. Starting again in the year 2000 and having to deal with all the major market storms, an investor owning the S&P 500 would finish 2022 with just $81,000. The same investor in a 60/40 portfolio would have $657,000. This chart from BlackRock illustrates the declines. 1

Source: BlackRock

The interesting piece to that chart is the top line or what BlackRock suggests doing. And that’s following an income-centric portfolio. Here, the investor’s portfolio would have grown from $1 million to $1.1 million, all while taking the $40,000 annual distributions.

Yield First

The key to BlackRock’s study is the strategy of investing solely for income during retirement and forgoing growth. In this case, they suggest a mix of one-third each of U.S. investment-grade bonds, high-yield bonds, and value/dividend stocks. Yields generated from these asset classes are enough to satisfy the need for income in retirement without having to sell assets. That’s critical because of the so-called sequence of withdrawal risks.

Those investors who retire at the wrong time essentially lock in losses, permanently reducing their balances. However, those who focus on yield and never have to touch the principal wins out. The best part is by following the two-pronged approach, investors would still have more than enough even with the decade of lower interest rates.

While some pundits have suggested this approach exposes you to interest rate risk, it’s less of a concern because the focus is on coupon rather than portfolio value. With bonds, you lock in yield when you make a purchase. Right now could be a great time for investors to do just that.

Following BlackRock’s Lead

With data suggesting that following an income-centric portfolio in retirement is best, investors just may want to follow BlackRock’s lead. That means focusing on growth till retirement and then switching to a yield-focused portfolio at retirement.

How do you create a yield-focused portfolio?

As we said before, BlackRock suggests a combination of investment-grade bonds, high-yield bonds, and value/dividend stocks. Using index ETFs, this portfolio can be achieved easily. In this case, that’s putting a third into the iShares Core U.S. Aggregate Bond ETF and iShares Broad USD High Yield Corporate Bond ETF. Then split the remaining third between the value and dividend ETFs, like the iShares Select Dividend ETF and iShares Core S&P U.S. Value ETF. This combination creates the yield needed for BlackRock’s income-centric portfolio to work.

But investors don’t have to be beholden to BlackRock or this model. Municipal bonds and investment-grade corporates could be added to help generate additional yield or add other opportunities. The idea is to focus on income first rather than growth.

BlackRock’s Income-Centric ETFs

These ETFs were selected based on their ability to provide low-cost exposure to BlackRock’s strategy for income. They are sorted by the YTD total return, which ranges from -2.5% to 16%. They have expenses between 0.03% and 0.61% and AUM between $120M and $91B. They are currently yielding between 2.2% and 6.5%.

| Ticker | Name | AUM | YTD Total Ret (%) | Yield (%) | Exp Ratio | Security Type | Actively Managed? |

|---|---|---|---|---|---|---|---|

| IUSV | iShares Core S&P U.S. Value ETF | $13.19B | 15.9% | 2.2% | 0.04% | ETF | No |

| USHY | iShares Broad USD High Yield Corporate Bond ETF | $9B | 8.6% | 6.5% | 0.22% | ETF | No |

| IYLD | iShares Morningstar Multi-Asset Income ETF | $124M | 7.3% | 6.2% | 0.61% | ETF | No |

| AGG | iShares Core U.S. Aggregate Bond ETF | $90.4B | 1.8% | 3.4% | 0.03% | ETF | No |

| DVY | iShares Select Dividend ETF | $17.11B | -2.5% | 4.1% | 0.38% | ETF | No |

The Bottom Line

Investors tend to include growth in their portfolios when they retire. However, that thinking could be wrong. According to BlackRock, income is what matters. Switching how we invest to a two-pronged approach of accumulation rather than income makes the most sense based on historical data.

1 BlackRock (August 2023). Why investors in retirement may want to consider an income approach